TL;DR:

- Small business owners often overlook the importance of legal entities, risking personal asset exposure.

- Forming and maintaining a proper legal structure provides liability protection, tax benefits, and business continuity.

- Consistent compliance and active management of the entity are vital to preserve its protections and benefits.

Most small business owners think legal entities are something only Fortune 500 companies worry about. That assumption is one of the most expensive mistakes you can make. Whether you run a one-person consulting practice or a five-employee retail shop, the structure you operate under determines how the law treats you when things go wrong, how much you pay in taxes, and whether a lawsuit can wipe out your personal savings. This guide breaks down exactly what a legal entity is, what types are available to you, and how to use that knowledge to make smarter, safer decisions for your business.

Table of Contents

- What is a legal entity?

- Types of legal entities for small businesses

- How legal entities protect you: Liability, tax, and compliance

- How to form and maintain a legal entity

- Our perspective: What most guides miss about legal entities

- Get help forming and managing your legal entity

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Legal entities separate your business | They give your business its own legal identity and protect your personal assets. |

| Choose the right type | LLCs, corporations, and partnerships each offer different protections and tax treatments. |

| Compliance is key | Maintaining registration, records, and filings preserves your legal protections over time. |

| Setup requires more than paperwork | Proper formation and ongoing diligence help avoid costly mistakes and legal risks. |

What is a legal entity?

At its core, a legal entity is any organization the law recognizes as having its own separate identity, apart from the people who own or run it. Think of it like this: when you form an LLC, you are essentially creating a new "person" in the eyes of the law. That new person can own property, sign contracts, open bank accounts, take on debt, and even get sued.

A legal entity, also known as a juridical or artificial person, is any non-human organization recognized by law as having a separate legal personality.

This stands in contrast to a natural person, which is just a human being. Natural persons have inherent legal personality from birth, while legal entities only gain that status through formal registration with the state.

So what can a legal entity actually do? Here is a straightforward breakdown:

- Own real estate and other property in its own name

- Enter contracts with vendors, employees, and customers

- Sue or be sued without involving your personal assets by default

- Open bank accounts and take on credit or debt

- Pay taxes separately from its owners (depending on entity type)

- Continue to exist even if ownership changes

The last point is surprisingly powerful. A legal entity has what lawyers call perpetual existence, meaning the business survives the departure or death of any one owner.

Not every business qualifies, though. A sole proprietorship, for example, is not a legal entity. If you freelance under your own name and never register anything, you and your business are one and the same in the eyes of the law. That means any business debt or lawsuit hits your personal finances directly. Understanding this distinction is step one in building a business that actually protects you.

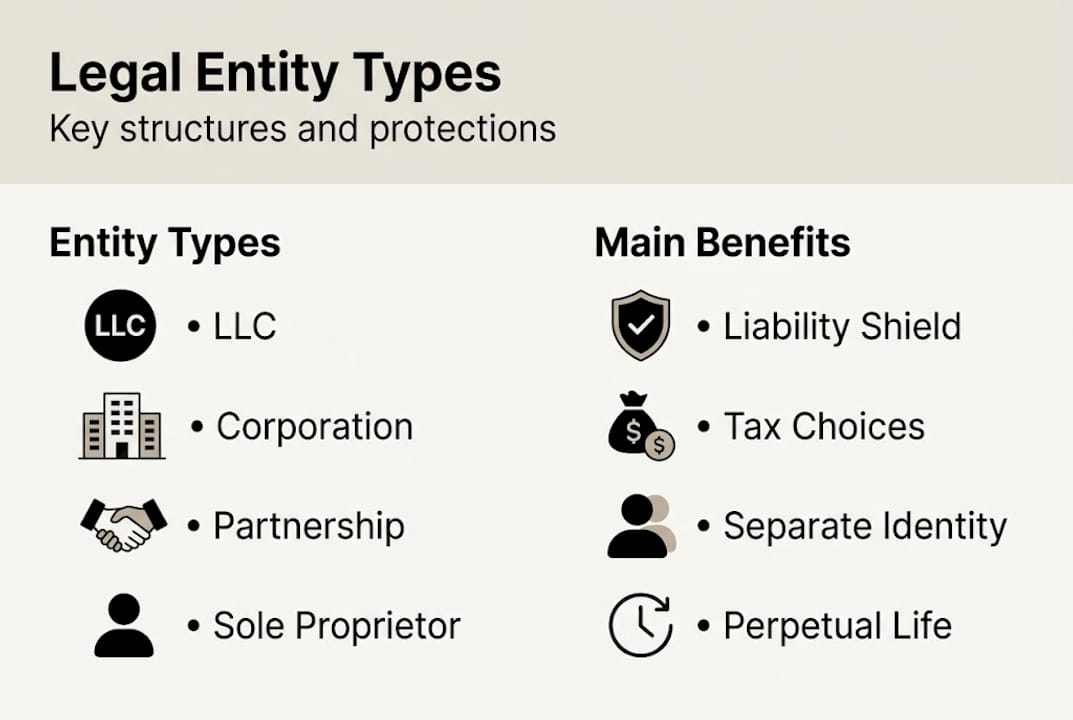

Types of legal entities for small businesses

Common types of legal entities for small businesses include LLCs, corporations (C-Corps and S-Corps), and partnerships. Each comes with different rules on liability, taxation, and administrative burden.

Here is a quick comparison to make the choice clearer:

| Entity type | Liability protection | Taxation | Paperwork burden |

|---|---|---|---|

| LLC | Yes | Pass-through (default) | Low to moderate |

| C-Corporation | Yes | Corporate + dividend tax | High |

| S-Corporation | Yes | Pass-through | Moderate to high |

| Partnership | Partial (varies) | Pass-through | Low to moderate |

| Sole proprietorship | None | Pass-through | Minimal |

Choosing the right structure depends heavily on your goals. Here is a quick guide:

- LLC: Best for most small businesses. Flexible management, limited legal risk protection, and simple taxation.

- C-Corporation: Best if you plan to raise venture capital or take the company public.

- S-Corporation: Great for small businesses that want corporate protection but prefer pass-through taxes, with IRS eligibility limits.

- Partnership (General or Limited): Works well for professional practices or co-owned ventures, but partners in a general partnership carry personal liability.

- Sole proprietorship: Easiest to start, but offers zero separation between you and the business.

Pro Tip: Do not just pick the cheapest or fastest option. Think about your industry risk, growth plans, and how many people will be involved. The importance of documentation from day one cannot be overstated because it directly determines how much protection you actually have.

How legal entities protect you: Liability, tax, and compliance

Here is where choosing the right entity stops being theoretical and starts saving or costing you real money.

Liability protection is the big one. When your business is a legal entity, creditors and plaintiffs generally cannot come after your personal home, car, or savings to satisfy business debts. LLCs offer liability protection and pass-through taxation; corporations provide strong protection but involve more formalities and potential double taxation.

For taxes, the difference is significant. Here is a simple breakdown:

| Tax model | Who pays | Entity types |

|---|---|---|

| Pass-through | Owners pay on personal returns | LLC, S-Corp, Partnership |

| Corporate taxation | Entity pays, then owners taxed on dividends | C-Corporation |

The [US tax code defines "person"](https://uscode.house.gov/view.xhtml?req=(title:26%20section:7701) to include individuals, trusts, estates, partnerships, associations, companies, and corporations, which is why the tax treatment explained for each entity type varies so widely. Understanding this before you file can prevent very costly surprises.

Compliance is the ongoing price of protection. Once you form an entity, you must:

- Appoint and maintain a registered agent in your state

- File annual reports with your state's secretary of state office

- Hold and document member or shareholder meetings (for corporations)

- Keep separate financial records for the business

- Renew any relevant business licenses or permits

Pro Tip: Neglecting these formalities can cause a court to "pierce the corporate veil," which means a judge can hold you personally responsible for business debts. Staying current with legal guidance for SMBs is not optional, it is your ongoing insurance policy.

How to form and maintain a legal entity

The actual process of forming a legal entity is more straightforward than most people expect. File articles of organization for an LLC or articles of incorporation for a corporation, appoint a registered agent, obtain an EIN, and draft bylaws. Costs typically run $50 to $500 or more depending on the state, and annual reports are required to maintain good standing.

Here is a step-by-step approach:

- Choose your entity type based on liability needs, tax preferences, and growth goals

- File your formation documents with your state (Articles of Organization for LLCs or Articles of Incorporation for corporations)

- Appoint a registered agent to receive official legal mail on behalf of the business

- Obtain an EIN (Employer Identification Number) from the IRS, which is free and takes minutes online

- Draft an Operating Agreement (LLC) or Bylaws (Corporation) to formalize ownership rules and decision-making

- Open a dedicated business bank account immediately, keeping finances completely separate from personal accounts

To draft foundational documents correctly from the start, templates and legal tech tools can reduce both time and cost significantly.

Avoid these common pitfalls after formation:

- Missing annual report deadlines, which can cause your entity to be dissolved by the state

- Co-mingling personal and business funds, which weakens your liability protection

- Failing to update records when ownership or addresses change

- Ignoring S-Corp election deadlines if you want special tax treatment

- Skipping the operating agreement because you think verbal agreements are enough

For compliance best practices and a thorough look at the essential compliance steps required in your state, reviewing your obligations annually is worth the effort. A step-by-step entity setup guide can also help you visualize the full process.

Pro Tip: If you are considering an S-Corp election or have multiple owners with unequal contributions, consult a licensed attorney or CPA before filing. Getting it right the first time is always cheaper than fixing it later.

Our perspective: What most guides miss about legal entities

Most articles on legal entities focus entirely on the formation process, and then they stop. That is the wrong place to stop. Formation is one afternoon's work. Maintenance is a forever commitment.

The real risk that ruins small businesses is not failing to form an entity. It is forming one and then treating it like a formality rather than a living, active structure. We see this pattern repeatedly. An owner forms an LLC, uses their personal account for business purchases "just this once," skips the annual report because they did not know it existed, and then discovers three years later that their liability shield has been quietly eroding the whole time.

The hidden risks of neglect are real and they are more common than any formation guide will tell you. Courts do pierce the corporate veil, and they do it more often when small businesses are involved because the informal habits are harder to avoid.

Our honest take: treat your legal entity like you treat your most important client. Set calendar reminders for renewal deadlines. Review your operating agreement every year. Keep your financials clean. These habits cost almost nothing and they protect everything.

Get help forming and managing your legal entity

Forming a legal entity is a significant step, and staying compliant once you do is an ongoing process that many small business owners underestimate.

BXP Legal AI simplifies this entire process, from helping you understand which entity type fits your situation to walking you through state-specific requirements. The platform offers ready-to-use legal templates for operating agreements, bylaws, and other foundational documents, along with multi-jurisdiction legal support for businesses that operate across state lines. Whether you are starting fresh or cleaning up an existing structure, BXP Legal AI gives you the guidance and tools you need without the typical attorney hourly rates.

Frequently asked questions

What makes a business a legal entity?

A business becomes a legal entity by formally registering with the state, which gives it a separate legal identity from its owners. You must file articles of organization or incorporation with the appropriate state office to complete this process.

Is a sole proprietorship a legal entity?

No. Sole proprietorships are not separate legal entities; the owner and the business are legally one and the same, meaning personal assets are fully exposed to business liabilities.

How do legal entities affect business taxes?

LLCs and partnerships typically pass profits directly to owners, who report them on personal returns, while corporations pay their own taxes and may result in double taxation when dividends are distributed.

What ongoing obligations do legal entities have?

Legal entities must file annual reports, pay state fees, and maintain accurate records to stay in good standing. Skipping these steps can lead to dissolution or loss of liability protection, with costs ranging from $50 to $500 or more annually depending on the state.

Can you change your business structure later?

Yes. Many businesses start as sole proprietorships and later convert to LLCs or corporations as they grow, though the conversion process involves new filings and potential tax implications.

Recommended

- Why small businesses need legal guidance: reduce risk

- Legal compliance explained: essential steps for SMBs

- Legal Risk Explained: Protect Your Business in 2026

- Multi-jurisdictional legal guide for SMBs in 2026

- Korp.ph | Complete Guide to Corporate Structures in the Philippines: Stock, Non-Stock, Foreign Entities, and Partnerships